The investment case for East African electric bus leasing

The investment case for East African electric bus leasing

Switching from fossil fuel to electric buses works well when you have cheap electricity, access to finance, limited behaviour change, and sufficiently short routes. East African capitals tick all these boxes and more. The market-leading electric bus leasing startup is BasiGo, a full-service leasing company with a similar business model to Zenobe in the UK or Highland in the US. Most investors are reluctant to take risks on new technologies in Africa, before they’ve matured elsewhere. Yet backers like MCJ, Mobility 54, Novastar and British International Investment (and even me as an angel investor) are bullish about BasiGo’s potential.

Nairobi is a hotbed of innovation in Africa, making it a very exciting place to start a business alongside other capitals like Kigali and Kampala. Motorbike electrification is a popular emerging markets electric vehicle opportunity because of low capital cost, short driving distances and the ease of charging and swapping out batteries. Nairobi hosts several EV start-ups, from equipment sales like Roam to motorbike battery swapping at Arc Ride. Zembo offers a similar product further afield in Uganda, and Kabisa in Rwanda operates their largest EV imports and charging network.

The impact potential of buses is also exciting. Due to the rising price of fuel, government data suggests that more Kenyans started using public transport in recent years, and there are thousands of diesel buses operating in the country.

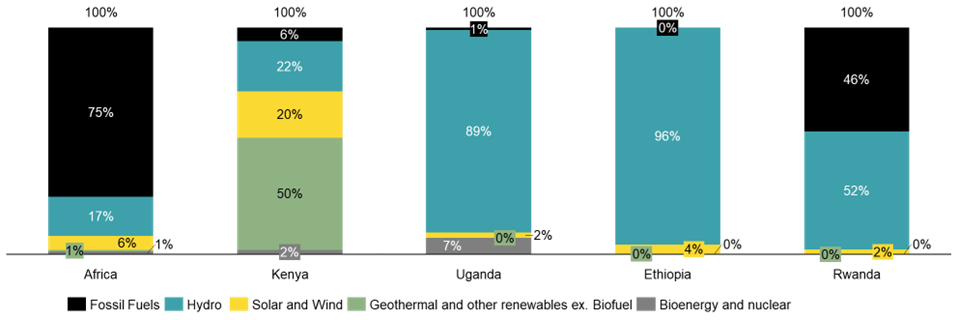

I’m sharing my investment thesis on electric bus leasing based on my infrastructure investing background, focusing primarily on BasiGo and Kenya given the availability of data. These themes also generally apply to other countries in East Africa with similarly green baseload power grids and informal bus systems, like Rwanda, Ethiopia, and Uganda.

Percent of energy production by source, Africa and selected countries, latest available (2023 Africa & Kenya, 2022 Uganda, Ethiopia, Rwanda)

Source: Ember

1. Buses can be powered by cheap electricity when no one else is using it

Electric buses typically have higher capital cost than a fossil-fuel bus, but if electricity costs are low enough, customers can save money by switching.

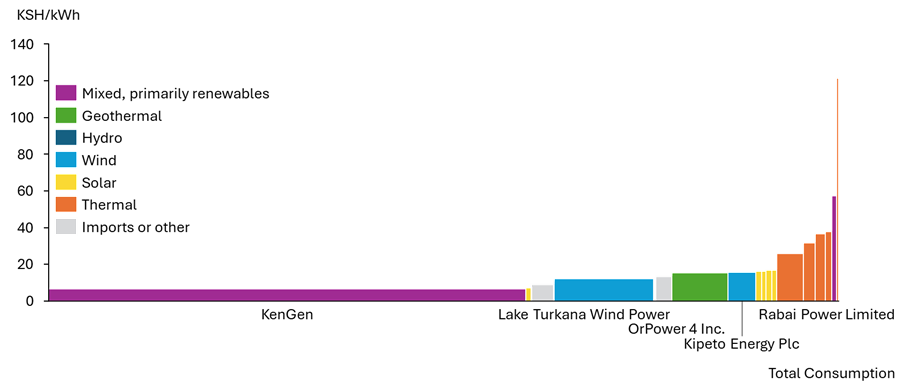

The Kenyan power grid is predominantly renewable, primarily through geothermal and hydroelectric generation. The cheapest power provider in Kenya is Kengen, a state-owned enterprise that provides over 60% of the country’s electricity. Kengen’s blended cost of electricity billed to Kenya’s utility, KPLC, is less than KSH 7 per kWh, or c. $0.048. Private sector projects like Kipeto Wind and OrPower are twice as expensive. Thermal energy for peak demand is 4 to 18 times more expensive, delivering only 7% of the total system’s energy need.

Cost to produce power by producer, Kenyan Shillings per kWh, 2023

Source: Data from KPLC Annual Filing, 2023; Cost analysis by Lucy Shaw

Geothermal and hydroelectric electricity are ‘baseload’ sources of energy, meaning they are available all day and night. Problematically, Kengen and KPLC do not have enough demand for this power in the evening, when business stops for the day. The capacity factor for these assets, a measure of the utilisation of the plant, is 77% for geothermal and 35% for hydro.

Even allowing for maintenance downtime, this leaves a large portion of potential energy production on the table. Kenya’s power contracts are sometimes structured using take-or-pay agreements, which means the utility pays for the power plant to be available regardless of whether they use the electricity. Being able to use as much electricity as they can in the evenings would reduce the blended cost of energy from those power stations.

What’s so great about electric buses for public transportation is they primarily charge at night. This is a win for both the bus operators and the utility. Electric buses can take advantage of cheaper baseload power in the evenings, and the utility can grow demand at a time when no one else is using power and make the most of their take-or-pay contracts.

2. Limited behavioural change is needed

BasiGo’s primary business model is leasing electric buses as a service (though they are also branching out into manufacturing). High capital costs and limited cost predictability for a new ‘fuel’ can deter adoption of electric vehicles, especially if the process to ‘refuel’ is also different.

BasiGo, like Zenobe and Highland, offers a financing, maintenance and charging package for companies, so that they can predict their recurring expenses and manage upfront costs.

For some bus systems, this is an unusual way of dealing with a bus supplier. They might be used to purchasing the bus outright, then managing their own fueling costs and processes themselves without any financing at all.

In Nairobi, though, the bus companies already take out credit to finance their buses, and thus are used to ongoing payments and dealing with banks. They also have a credit profile based on their ability to manage similar prior payments.

Kenyan buses are typically fuelled when they are parked in a depot near a petrol station at night, ready for the day ahead. Instead, these buses can be parked at electric charging depots, or chargers can be installed in existing carparks. BasiGo ran tests prior to launch that showed the bus range on a single charge could manage most of the mutatu routes for the day, and they also offer the option to charge buses during the day if needed.

Bus network operators thus do not have to deal with as much inconvenience from behavioural change when switching to electric vehicles. BasiGo’s pitch becomes one of cost, predictability and quality instead.

3. Privatised, numerous counterparties diversify risk

One risk with infrastructure investing in Africa is that you only have one customer: the government. While governments can be great counterparties, with predictable needs and higher investment grades than businesses, this can be a major risk for a company. There are no other customers that can absorb your services if the government decides not to pay, or to vigorously renegotiate terms.

The benefit of launching an electric bus company in Kenya is the magic of mutatus, the vibrantly colourful buses that are the lifeblood of the city. These are owned by private operators, typically large savings and credit cooperatives (SACCOs). There are many of these companies, of various sizes. Selling or leasing buses to a larger number of customers diversifies the risk from customers defaulting, and means that a company can be selective about who it negotiates contracts with.

Challenges

Of course, almost no investment is without risk - like many companies operating in Africa, currency devaluations, procurement delays and high financing costs are a challenge. Despite Kenya’s usually supportive business environment, there is also a risk of government intervention in the infrastructure sector, for example in raising electricity prices or import tariffs. Given the value that electric vehicles provide to the government and its state-owned enterprises, this risk is partially, but not fully, mitigated.

While Kenya introduced heavily discounted EV electricity rates, they have also proposed to raise tariffs on imports this May, which reduces the attractiveness of a capital-intensive business model. This is partly because the government is under pressure to balance its budget for an IMF program, but also to incentivise local manufacturing and assembly. Companies like BasiGo are looking to manufacture locally to reduce costs relative to imports and further support Kenyan economic development.

Another issue is working with a relatively new technology in a higher risk market, especially with limited servicing capabilities and lower quality roads. During BasiGo’s testing, the buses held up well, even driving over Nairobi potholes. Being vertically integrated and offering value-added services also helps to build a competitive moat around their offering, making it more likely that they will generate repeat business and maintain contracts with customers. This will help them as they look to raise further capital, as their business will be more appealing to infrastructure investors, who have a lower cost of capital.

Despite these risks, I’m bullish on Kenya’s electric vehicle potential, at least in the public transport sector. The fundamental conditions exist for this to become the dominant low-carbon transport technology in Nairobi and perhaps the entire East African region.